Bull Case For The Trade Desk (TTD)

The Trade Desk (TTD) represents an interesting long-term investment opportunity following its recent steep decline, driven by an overreaction to short-term earnings disappointment rather than a deterioration in its core business. With a robust growth trajectory, leadership in programmatic advertising, and favorable secular tailwinds, TTD is undervalued at current levels, offering potential upside for patient investors. As a bonus for covered call writers, the weekly call options pay well, too.

TTD Stock Price Last 12 Months

The Trade Desk is a leading independent demand-side platform (DSP) in the digital advertising ecosystem. Its stock plummeted over 30% this month following its Q4 2024 earnings release. The drop erased approximately $16 billion in market value, bringing the share price to around $75 as of February 25, 2025. The sell-off was triggered by a rare revenue miss (of 2%) — the first in the company’s 8-year public history — and a weaker-than-expected Q1 2025 guidance, which spooked investors accustomed to consistent outperformance. However, the underlying business remains strong.

Currently, broader market dynamics are influencing high-growth tech stocks like TTD. The Nasdaq Composite has faced downward pressure, reflecting a risk-off sentiment among investors amid rising treasury yields and macroeconomic uncertainty. Growth stocks, particularly those with high valuations, have been hit hard as interest rates fluctuate and investors rotate into value or defensive sectors. This environment has amplified the negative reaction to TTD’s earnings miss, with high-beta names bearing the brunt of the sell-off. However, the decline in TTD appears disproportionate to its fundamentals, suggesting an overreaction that creates a buying opportunity.

Bull Case for TTD

- Intact Long-Term Growth Story Despite the Q4 stumble, TTD delivered full-year 2024 revenue of $2.44 billion, up 26% year-over-year, with EBITDA exceeding $1 billion at a 41% margin. The company remains a “Rule of 50” business (revenue growth + free cash flow margin > 50%), generating $630 million in free cash flow in 2024. Management’s guidance for Q1 2025, while conservative, still implies double-digit growth. The programmatic advertising market, particularly in connected TV (CTV), continues to expand rapidly, and TTD’s leadership position in this high-growth segment—bolstered by partnerships with Disney, Netflix, and others—positions it to capture significant share as ad budgets shift from linear TV to digital.

- Attractive Valuation Post-Drop At $75, TTD trades at approximately 45x forward earnings, a sharp discount from its pre-earnings multiple of 60x and its five-year average of 86x. The stock’s PEG ratio (price-to-earnings-to-growth) now sits at 1.9x, 35% below its historical average, indicating that the market has overly discounted its growth potential.

- Strong Financial Position TTD boasts a strong balance sheet with $1.9 billion in cash and no debt, providing flexibility to navigate short-term headwinds and invest in growth. The newly announced $1 billion share repurchase program signals management’s confidence in the stock’s undervaluation and helps offset dilution from stock-based compensation, which, while high at 17.4% of revenue, has been trending downward.

- Secular Tailwinds and Competitive Moat The shift to digital advertising, accelerated by cord-cutting and the rise of ad-supported streaming, plays directly into TTD’s strengths. Unlike walled gardens like Google and Meta, TTD’s focus on the open internet and its agnostic, data-driven platform gives it a unique edge. Innovations like Unified ID 2.0 and partnerships with publishers via OpenPath further solidify its moat, ensuring relevance as third-party cookies phase out.

- Market Overreaction Creates Opportunity The steep drop reflects a punishment for perfection rather than a structural flaw. Sentiment on platforms like X highlights oversold conditions, with some analysts and traders calling for a reversal as the stock nears technical support levels (e.g., $70-$72). Historically, TTD has rebounded from volatility tied to broader market corrections, rewarding investors who buy the dip.

Baby and the Bath Water

The Trade Desk’s recent drop is a classic case of the market throwing out the baby with the bathwater. While near-term uncertainty persists, the company’s fundamentals—growth, profitability, and market position—remain intact. Current market conditions have exaggerated the sell-off, driving TTD to an attractive valuation for long-term investors. TTD remains a best-in-class name in a secularly growing industry, and this dip is a rare chance to buy at a discount.

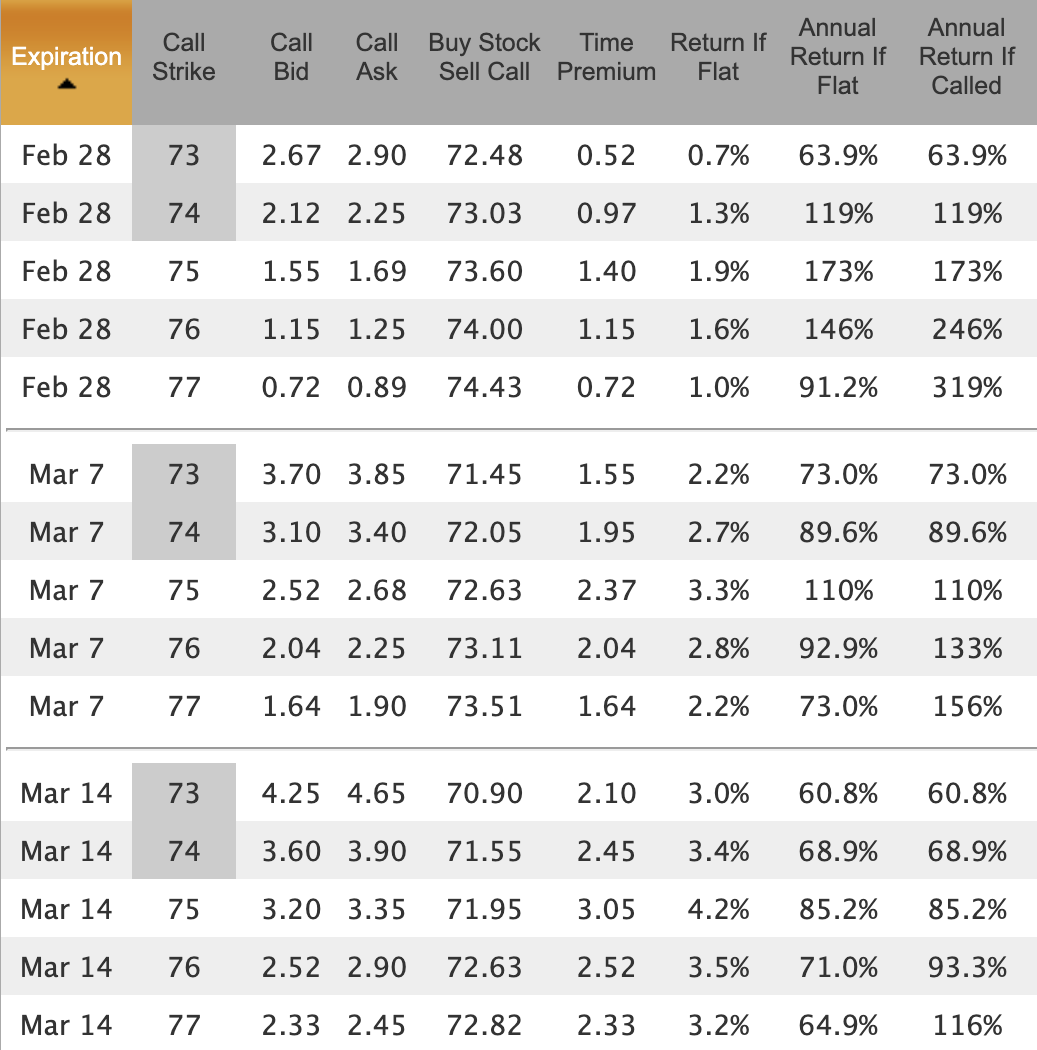

Weekly TTD Covered Call Examples

Searching for deep in the money covered calls? Check out our Covered Call Screener

Mike Scanlin is the founder of Born To Sell and has been writing covered calls for a long time.