Qualified Dividends

Disclaimer: We are not tax accountants. This is our layperson interpretation of the rules. Consult your tax advisor.

For investors who write covered calls on dividend paying stocks in taxable accounts, it’s important to know the distinction between a “qualified” and “unqualified” dividend (but if you’re investing in a tax-deferred account (eg. an IRA account) you can ignore this).

Since 2003 dividends have been federally taxed at ordinary income rates, as opposed to lower long-term capital gains rates. But some dividends are special, or “qualified”, for a lower tax rate. This is a good thing, and if you can swing it you’d rather have your dividends be qualified instead of unqualified, because it will lower your taxes.

What makes a dividend qualified?

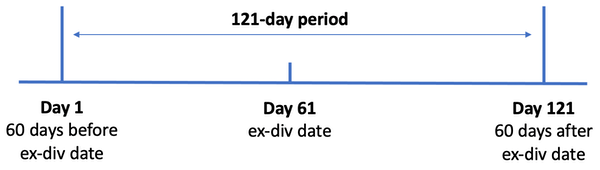

The IRS considers a dividend qualified if you have held the underlying stock more than 60 days during the 121-day period that begins 60 days before the ex-dividend date. So, visually:

Unqualified Dividend Example

Imagine you bought XYZ stock on July 5 and it paid a cash dividend of 10 cents with an ex-dividend date of July 12. You sold the shares on August 8, so you held your shares for 34 days of the 121-day period (from July 6 through August 8). The 121-day period began on May 13 (60 days before the ex-dividend date) and ended on September 10. You have no qualified dividends from XYZ because you held XYZ stock for less than 61 days during the relevant period.

Qualified Dividend Example

Assume the same facts as above except that you bought the stock on July 11 (the day before the ex-dividend date) and you sold the stock on September 13. You held the stock for 63 days (from July 12 through September 13). The dividends are qualified dividends because you held the stock for 61 days of the 121-day period (from July 12 through September 13).

When counting days you include the day you sold the stock but not the day you acquired it. And your days do not need to be contiguous. Any 60 days during that period will work.

Exclusions To Holding Period

The IRS doesn’t want you to count any days where your risk of loss is diminished. They define “diminished risk” as:

- You had an option to sell, were under a contractual obligation to sell, or had made (and not closed) a short sale of substantially identical stock or securities.

- You were grantor (writer) of an option to buy substantially identical stock or securities.

- Your risk of loss is diminished by holding one or more other positions in substantially similar or related property.

So, (1) says that days you own a put option on the stock don’t count. And (2) says you can’t count days where you have written a call option on the stock. While (3) is a catch all to cover other cases.

Basically, the IRS doesn’t want investors to get preferential tax treatment for any strategy where they get the dividend but don’t have normal risk for the underlying stock position. Obviously, if options are involved then the choice of strike price matters, because deep in the money options have a different "diminished risk" profile than out of the money options.

Qualified Dividends With Covered Calls

From what we’ve read, covered call writers can continue their holding period if they’re writing at-the-money or out-of-the-money options against their stock where the expirations are longer than 30 days when they sell the option. But writing short-term options (less than 30 days) or in-the-money covered calls will suspend the holding period if they are in-the-money by more than 1 strike price.

Note: These tax rules were written years ago when there were fewer strikes. It would make more sense to express the moneyness of an option as a % of the underlying stock price, but alas, the tax code does not always make sense. “One strike in-the-money” does not mean the same thing for TSLA where strikes are every 2.5 points (about 0.3% of the underlying price) vs X where strikes are every 0.5 points (about 3% of the underlying price). Surely 3% ITM on X is not the same risk profile as 0.3% ITM on TSLA.

Super Fun Record Keeping

Now, in reality no-one tracks their dividends or stock purchases/sales with 121-day windows in mind. Don’t worry, your broker does it for you and prepares your 1099-DIV accordingly. But if your holding period is around 2 months and a dividend was paid during that time, it might be worth thinking about it a little (the same way knowing if your holding period is more or less that 12 months for long-term vs short-term capital gains on the stock). Holding the stock a few more days might make the difference between a qualified dividend and an unqualified dividend.

How much difference can it make?

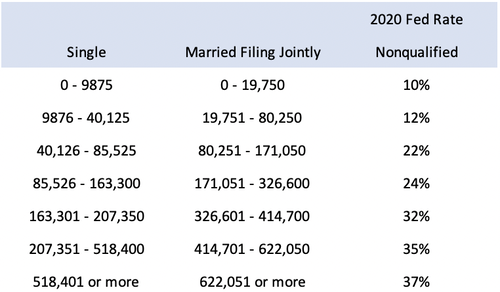

First we have to look at the federal ordinary income brackets for 2020, which is what you pay on unqualified dividends:

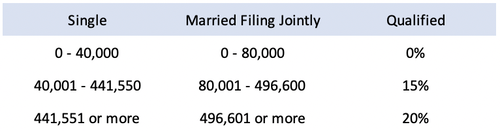

The brackets for qualified dividends are (of course) different. Here’s what you pay at the federal level for qualified dividends:

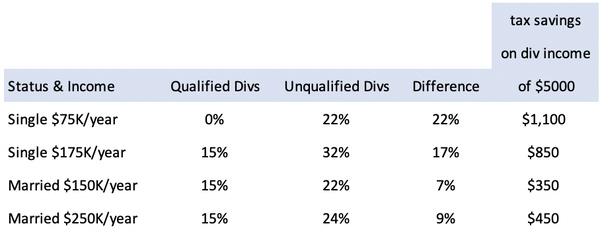

So, if we bring it all together and look at a couple of single filer examples, and a couple of married filer examples, here’s the actual difference in tax paid on $5000 of qualified vs unqualified dividends:

So, if you’re single making $75K/year you can save 22% tax on your dividend income if you make sure they are all qualified. That’s over $1000 in tax savings in our example where you earn $5000 of dividends during the year.

But the bottom line is that many covered call investors implement a dividend capture strategy with trades that do not meet the holding requirement. Either because they are writing calls that are more than 1 strike in-the-money, less than 30 days in duration, or because they don’t hold the stock for 60 days. Nothing wrong with any of that but, if trading in a taxable account, all your dividends will be taxed as ordinary income.

If you are a buy-and-hold investor with a covered call overwrite strategy (selling out of the money options against your shares) where you sell options more than 30 days out on shares you don't trade more than once every 60 days, then you should be fine. Meaning, any dividends you receive should be qualified.

If you really want to get into the rules more, check out Fidelity’s article Tax implications of covered calls or, better yet, consult with your tax advisor.

Mike Scanlin is the founder of Born To Sell and has been writing covered calls for a long time.